Introduction

Many of the world's best-educated professionals dabble in markets and still make the same mistakes as casual speculators. Finance textbooks teach that investors should rationally trade off risk and return, diversify broadly and follow the law of large numbers. Yet actual behaviour often deviates from this ideal. Behavioural finance explores why--showing that cognitive shortcuts and emotional responses distort how people perceive risk and lead them to gamble badly in trading. This article unpacks the psychological biases that ensnare even the smartest traders and outlines strategies to avoid them.

Rational theory vs. real behaviour

Traditional finance assumes that investors are rational and markets are efficient. Behavioural research has exposed a wide gap between this theory and reality. Studies of individual equity investors show that heuristic biases--overconfidence, representativeness, availability, anchoring and the gambler's fallacy--shape investment decisions. Risk perception, a subjective judgment about the probability and severity of a loss, mediates the relationship between these biases and the choice to invest. When participants in one survey were asked about their trading at India's National Stock Exchange, their perception of risk partially explained why overconfidence, availability and gambler's-fallacy beliefs led them to buy or sell. In other words, what people feel about risk matters as much as what they know.

Biases that lead smart traders astray

Overconfidence

Overconfidence describes the tendency to overestimate one's knowledge, predictive ability or control over outcomes. Behavioural experiments find that overconfident investors trade more frequently and ignore contradictory information. In a survey of equity investors, overconfidence was one of the strongest predictors of risky investment decisions. Because overconfident traders believe their opinions are superior, they often fail to diversify and can suffer lower returns.

Loss aversion

Prospect theory shows that people dislike losses more than they enjoy equivalent gains. This loss aversion bias causes investors to hold losing positions too long and sell winners too early. Loss-averse traders may avoid equities altogether after experiencing a downturn, missing out on future growth. Experiments reveal that when participants face sustained losses, loss aversion can override early optimism and lead to risk-seeking to "break even," increasing volatility and potential losses.

Anchoring and availability

Anchoring occurs when people fixate on an arbitrary reference point, such as a stock's historical high, and fail to adjust their expectations with new information. Availability bias leads investors to rely on easily recalled events--recent news or personal experiences--rather than a comprehensive analysis. When information is readily available, investors overweight its importance and may overreact to recent events. Both biases cause mispricing and can generate momentum and reversals in markets.

The gambler's fallacy and hot-hand belief

The gambler's fallacy is the belief that a random event is "due" to happen because it hasn't occurred recently. A 1913 run of twenty-six blacks in a row at Monte Carlo led gamblers to bet heavily on red, only to lose fortunes when black continued. Modern investors make similar mistakes. In an experiment where participants bet on coin tosses or followed random "experts," those making their own bets showed gambler's-fallacy behaviour: the frequency of betting on heads (or tails) decreased after streaks of the same outcome. Investopedia notes that the fallacy incorrectly assumes future random events are influenced by past events. Even sophisticated traders misinterpret streaks of market gains or losses, selling after a series of wins or buying after a series of losses.

Interestingly, neuroscience suggests that smart people are not immune. A study of 438 college students found that use of the gambler's-fallacy strategy correlated positively with general intelligence and executive functions but negatively with affective decision-making capacity. Participants with strong cognitive abilities but weak emotional systems were more prone to the fallacy. This finding implies that intelligent traders may be better at spotting patterns but worse at relying on intuitive "gut" signals when those patterns are meaningless.

Illusion of control

The illusion of control bias leads investors to overestimate their ability to influence outcomes. Investopedia defines it as a cognitive bias where people believe they can control events that are actually uncertain. In finance, this bias manifests when analysts believe they can pick stocks or time the market through research, or when day traders think frequent trades give them control. The illusion of control contributes to overtrading, portfolio concentration and risky decision-making. To mitigate it, experts recommend diversification, a long-term horizon and adherence to evidence-based strategies.

House money effect

After a winning trade, investors often feel they are playing with "found money." The house money effect, named after casino terminology, describes the tendency to take on greater risk when reinvesting profits than when investing one's own savings. According to behavioural finance research, investors consider recent profits separate from earned income and therefore invest them with higher risk tolerance. This misclassification of capital leads traders to buy higher-beta stocks or pursue riskier strategies after profitable trades. The effect arises from mental accounting--the idea that money in different "mental accounts" is treated differently--and can expose investors to larger drawdowns.

Herd behaviour

Herd behaviour is the tendency to mimic the actions of a larger group, regardless of one's own information. During bull markets or panics, social and informational pressures cause investors to follow the crowd, contributing to bubbles and crashes. This bias explains why speculative frenzies occur even when individuals privately believe prices are unjustified.

Table: Cognitive biases that distort risk

| Bias | Description | Impact on trading |

|---|---|---|

| Overconfidence | Belief that one's skills and information are superior; underestimates uncertainty | Leads to excessive trading, under-diversification and ignoring contradictory data |

| Loss aversion | Losses feel more painful than equivalent gains | Traders hold losing positions too long and sell winners too early, avoiding losses rather than maximizing returns |

| Anchoring | Fixating on arbitrary reference points (e.g., past prices) | Causes investors to stick to outdated expectations and misprice assets |

| Availability bias | Relying on easily recalled information rather than all relevant data | Overreacts to recent news and personal experiences, leading to momentum and reversals |

| Gambler's fallacy | Belief that random events will "balance out," making streaks less likely | Investors misinterpret streaks of gains or losses and make poor timing decisions |

| Illusion of control | Overestimating one's ability to control uncertain outcomes | Leads to overtrading, concentrated positions and risky speculation |

| House money effect | Treating profits as separate from principal, leading to higher risk tolerance | Encourages riskier trades after gains and exposes investors to larger drawdowns |

| Herd behaviour | Mimicking the crowd despite contrary information | Contributes to bubbles and crashes as investors follow others into risky trades |

Table 1. Summary of the cognitive biases discussed in this article and their typical impact on trading behavior.

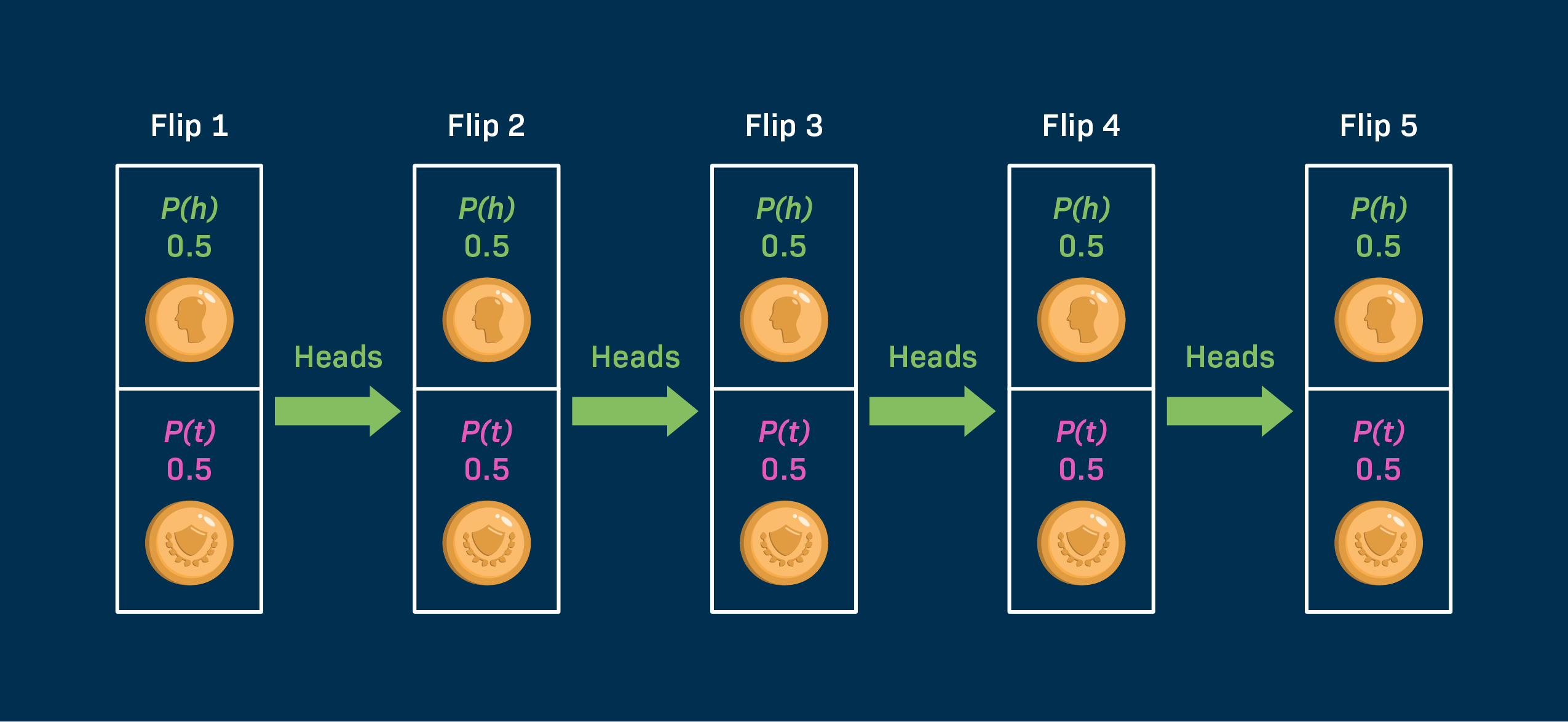

Figure 1. A coin-flip streak visualization showing why streaks do not change underlying probabilities, a common source of gambler's-fallacy thinking.

Figure 2. A mental-accounts diagram illustrating how profits are separated from principal, which increases risk tolerance and produces the house money effect.

Risk perception and tolerance

Risk perception is a biased judgment about the severity and probability of losses. It encompasses attitudes, beliefs, feelings and social values. When individuals perceive they have no control over outcomes, they view all risks as chance events. Investors may therefore label equity investing as "risky" regardless of the expected return. Perceived risk influences risk tolerance: after experiencing profits, traders' tolerance rises (house money effect), while after losses, loss aversion makes them more cautious or more desperate to "break even." Risk perception also mediates the effect of heuristics; overconfident or availability-driven investors take greater risks partly because they downplay perceived dangers.

Why intelligence isn't enough

The experimental findings on the gambler's fallacy highlight a paradox: individuals with higher cognitive ability may be more susceptible to certain biases. Smart traders excel at spotting patterns and using complex models, yet those skills can backfire when markets are random. High intelligence does not prevent emotional responses such as regret, fear or euphoria. In fact, the strong executive function that helps detect patterns can reinforce the illusory patterns that underlie the gambler's fallacy. Meanwhile, affective decision-making capacity--the ability to use emotional signals to guide choices--protects against the fallacy. Intelligence without emotional regulation may therefore increase vulnerability to risk misperceptions.

Strategies to avoid psychological pitfalls

Knowing these biases is a first step toward better trading decisions. The following strategies can mitigate their impact:

| Strategy | Explanation |

|---|---|

| Develop a rules-based system | Use predefined buy/sell signals and position sizes rather than gut instinct. Traders aware of the gambler's fallacy can avoid it by following systems based on independent research. |

| Diversify and rebalance | Spread investments across asset classes and rebalance periodically to reduce concentrated risk. Diversification counters the illusion of control and limits the impact of availability and anchoring biases. |

| Adopt a long-term perspective | Focus on long-term goals and avoid frequent trading. This reduces overtrading and house money tendencies. |

| Record and review trades | Keep a trading journal to track decisions, emotions and outcomes. Reviewing past trades helps identify biases and correct them. |

| Use stop-loss and position sizing | Setting stop-loss orders and sizing positions conservatively protects against loss aversion and the disposition effect. |

| Seek independent advice | Consult financial advisors or robo-advisors to counteract personal biases. External perspectives can temper overconfidence and herd behaviour. |

| Educate yourself on behavioural finance | Awareness of cognitive biases, such as confirmation bias and the illusion of control, helps investors recognize when they are being influenced. |

Conclusion

Risk is inherent in investing, but poor risk perception and cognitive biases can amplify that risk. Smart people gamble badly not because they lack knowledge but because heuristics and emotions distort their understanding of probability and value. Overconfidence, loss aversion, anchoring, availability, the gambler's fallacy, the illusion of control, house money effects and herd behaviour all contribute to systematic misjudgments. Intelligence may even increase susceptibility when pattern-seeking overpowers emotional cues. By recognizing these biases and adopting disciplined strategies--diversification, rules-based trading, long-term focus and continuous learning--investors can improve their decision-making. Ultimately, the psychology of risk reminds us that trading is as much about managing ourselves as it is about managing our portfolios.

References

- Heuristic Biases as Mental Shortcuts to Investment Decision-Making: A Mediation Analysis of Risk Perception | MDPI

- Behavioral Finance and Investor Psychology: Examining the Role of Cognitive Biases in Stock Market Fluctuations

- The Hot Hand Belief and the Gambler's Fallacy in Investment Decisions under Risk | Request PDF

- The Gambler's Fallacy: Key Examples and Impact

- The Gambler's Fallacy Is Associated with Weak Affective Decision Making but Strong Cognitive Ability - PMC

- Illusion of Control Bias: What It Is and How It Can Impact Investment Returns

- House Money Effect: Meaning, Examples and FAQs

- LabXchange Independent probabilities